Choosing the right life insurance policy is a crucial financial decision that impacts your family’s future security. Among the various options available, Term Insurance and Whole Life Insurance are the two most popular types. While both provide life cover, they differ significantly in cost, duration, benefits, and purpose.

In this SEO-friendly guide, we’ll break down Term Insurance vs Whole Life Insurance in simple terms to help you decide which policy best suits your needs.

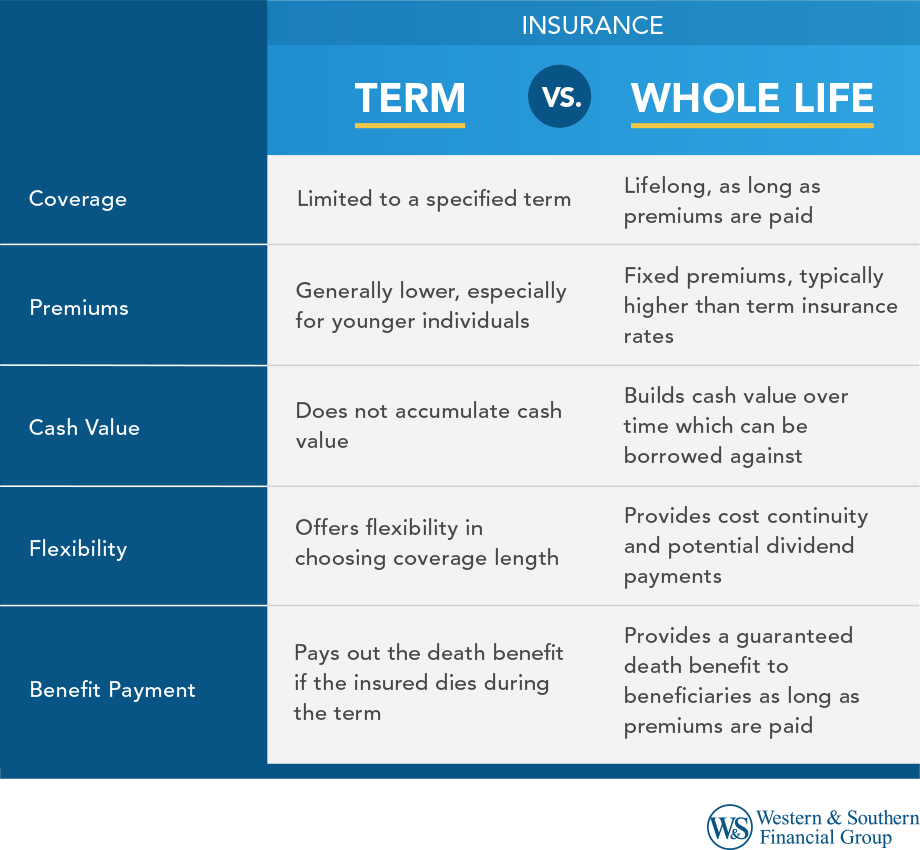

What Is Term Insurance?

Term Insurance is a pure life insurance plan that provides coverage for a specific period, known as the policy term (for example, 10, 20, or 30 years).

If the policyholder passes away during the term, the nominee receives the sum assured. However, if the policyholder survives the term, no maturity benefit is paid (unless it’s a return-of-premium variant).

Key Features of Term Insurance

- Affordable premiums

- High life cover at low cost

- Fixed policy duration

- Ideal for income replacement

Pros of Term Insurance

- ✔ Best for financial protection

- ✔ Suitable for young earners and families

- ✔ Simple and transparent

Cons of Term Insurance

- ✘ No savings or investment component

- ✘ No payout if the policyholder survives the term

What Is Whole Life Insurance?

Whole Life Insurance provides life coverage for the entire lifetime of the policyholder (usually up to 99 or 100 years). Along with insurance protection, it also includes a savings or investment component, known as cash value.

The policy pays a death benefit whenever the policyholder passes away, and in some cases, also offers maturity benefits.

Key Features of Whole Life Insurance

- Lifelong coverage

- Savings + insurance combined

- Cash value accumulation

- Higher premiums

Pros of Whole Life Insurance

- ✔ Lifetime financial security

- ✔ Acts as a long-term savings tool

- ✔ Cash value can be borrowed against

Cons of Whole Life Insurance

- ✘ Expensive compared to term plans

- ✘ Lower returns compared to other investments

Term Insurance vs Whole Life Insurance: Comparison Table

| Feature | Term Insurance | Whole Life Insurance |

|---|---|---|

| Coverage Duration | Fixed term (10–40 years) | Lifetime |

| Premium Cost | Low | High |

| Maturity Benefit | No | Yes (in many plans) |

| Savings Component | ❌ No | ✔ Yes |

| Ideal For | Protection-focused buyers | Long-term planners |

Which Is Better: Term Insurance or Whole Life Insurance?

The answer depends on your financial goals, age, and responsibilities.

Choose Term Insurance if:

- You want maximum coverage at minimum cost

- You are the primary earning member of your family

- You have short-to-medium-term liabilities (loans, children’s education)

Choose Whole Life Insurance if:

- You want lifelong coverage

- You are looking for insurance + savings in one product

- You want to leave a guaranteed inheritance

Can You Have Both?

Yes! Many financial experts recommend combining both:

- Term Insurance for high-risk protection

- Whole Life Insurance for long-term wealth planning

This balanced approach ensures both security and savings.

Final Thoughts

When comparing Term Insurance vs Whole Life Insurance, there is no one-size-fits-all answer. Term insurance is best for pure protection, while whole life insurance suits those looking for lifelong coverage with a savings element.

Before buying, assess your income, dependents, long-term goals, and budget. Making the right choice today can secure your family’s financial future tomorrow.