Life insurance is one of the most important financial tools for protecting your family’s future. Yet, one common question confuses most people: How much life insurance do you really need? Buying too little can leave your loved ones financially vulnerable, while buying too much can strain your budget.

This SEO-friendly guide breaks down life insurance coverage in a simple, practical way so you can choose the right amount with confidence.

Why Calculating the Right Life Insurance Amount Matters

Life insurance is not a one-size-fits-all product. Your ideal coverage depends on:

- Your income and expenses

- Family size and lifestyle

- Outstanding loans and future goals

The right coverage ensures your family can maintain their lifestyle, pay off debts, and achieve long-term goals even in your absence.

The Basic Rule: Income Replacement Method

A popular and easy way to estimate coverage is the income replacement method.

Formula:

Life Insurance = 10–15 × Annual Income

Example:

If you earn ₹6 lakh per year:

- Minimum coverage: ₹60 lakh

- Ideal coverage: ₹90 lakh

This method works well for salaried individuals but does not account for debts or future expenses, so let’s go deeper.

Factors That Decide How Much Life Insurance You Need

1. Your Dependents

The number of people financially dependent on you plays a crucial role:

- Spouse

- Children

- Dependent parents

More dependents = higher coverage needed.

2. Outstanding Liabilities

Your life insurance should clear all major debts, such as:

- Home loan

- Personal loan

- Car loan

- Credit card dues

This ensures your family is not burdened with repayments.

3. Daily Living Expenses

Calculate monthly household expenses and multiply them by the number of years your family will need support.

Example:

Monthly expenses: ₹30,000

Annual expenses: ₹3.6 lakh

Support for 20 years = ₹72 lakh

4. Children’s Education & Marriage

Future milestones are expensive and should be included:

- School & college education

- Professional courses

- Marriage expenses

Planning for these ensures your children’s dreams are not compromised.

5. Existing Savings & Investments

Deduct what you already have:

- Fixed deposits

- Mutual funds

- EPF/PPF

- Other life insurance policies

Life insurance should fill the gap, not duplicate existing assets.

The Human Life Value (HLV) Method

The Human Life Value approach calculates insurance based on your economic value over your working years.

It considers:

- Current income

- Future income growth

- Retirement age

- Inflation

This method is more accurate and ideal for long-term planning.

Life Insurance Coverage by Life Stage

For Young Singles

- Coverage: 8–10× income

- Focus on affordability and long-term policies

For Married Individuals

- Coverage: 10–15× income

- Add spouse and shared liabilities

For Parents

- Coverage: 15–20× income

- Include children’s education and lifestyle costs

For Near-Retirement Individuals

- Coverage depends on liabilities

- Lower coverage if children are financially independent

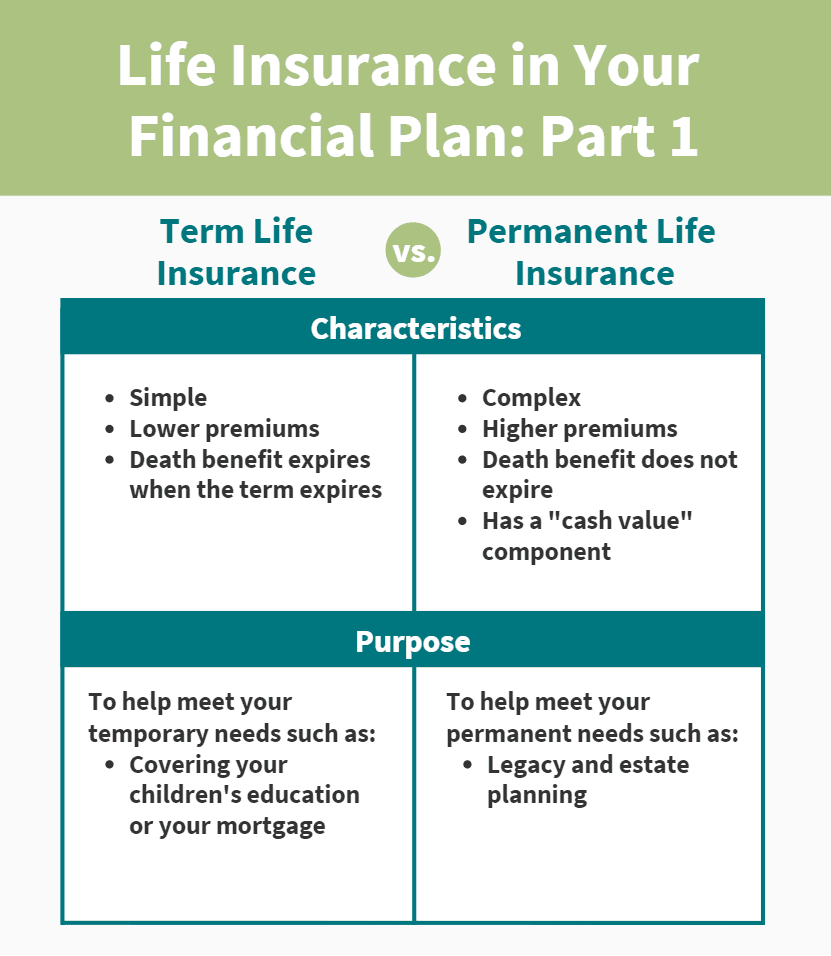

Term Insurance: Best Option for Adequate Coverage

If your goal is high coverage at low cost, term insurance is usually the best choice. It offers:

- Large coverage amounts

- Affordable premiums

- Pure protection without investment components

This makes it ideal for income replacement and family security.

Common Mistakes to Avoid

- Underestimating future expenses

- Ignoring inflation

- Relying only on employer-provided insurance

- Not reviewing coverage after major life events

Reassess your life insurance whenever you marry, have children, or take on major loans.

Final Thoughts: How Much Life Insurance Is Enough?

The right life insurance amount is one that:

- Replaces your income

- Clears all debts

- Secures your family’s future goals

A good starting point is 10–15 times your annual income, adjusted for liabilities and long-term needs. Taking time to calculate your coverage today can provide lifelong peace of mind for your loved ones.

Tip: Use an online life insurance calculator or consult a financial advisor to fine-tune your coverage accurately.