Missing an insurance premium payment is more common than you might think. A busy schedule, financial stress, or simply forgetting the due date can lead to missed payments. But what actually happens if you don’t pay your insurance premium on time? Does your policy get canceled immediately, or do you have some flexibility?

In this SEO-friendly guide, we’ll explain the consequences of missed insurance premium payments, grace periods, policy lapses, revival options, and how you can avoid such situations in the future.

What Is an Insurance Premium?

An insurance premium is the amount you pay (monthly, quarterly, half-yearly, or annually) to keep your insurance policy active. It applies to all types of insurance, including:

- Life insurance

- Health insurance

- Motor insurance

- Term insurance

- Travel insurance

Paying premiums on time ensures continuous coverage and financial protection.

What Happens If You Miss an Insurance Premium Payment?

The impact of a missed premium depends on the type of insurance and how long the payment is delayed. Below are the most common outcomes.

1. Grace Period: Temporary Relief

Most insurance policies come with a grace period, which is extra time allowed after the due date to pay your premium without losing coverage.

Typical grace periods:

- Life insurance: 15–30 days

- Health insurance: 15–30 days

- Motor insurance: Usually very short or none

👉 Important: During the grace period, your policy generally remains active.

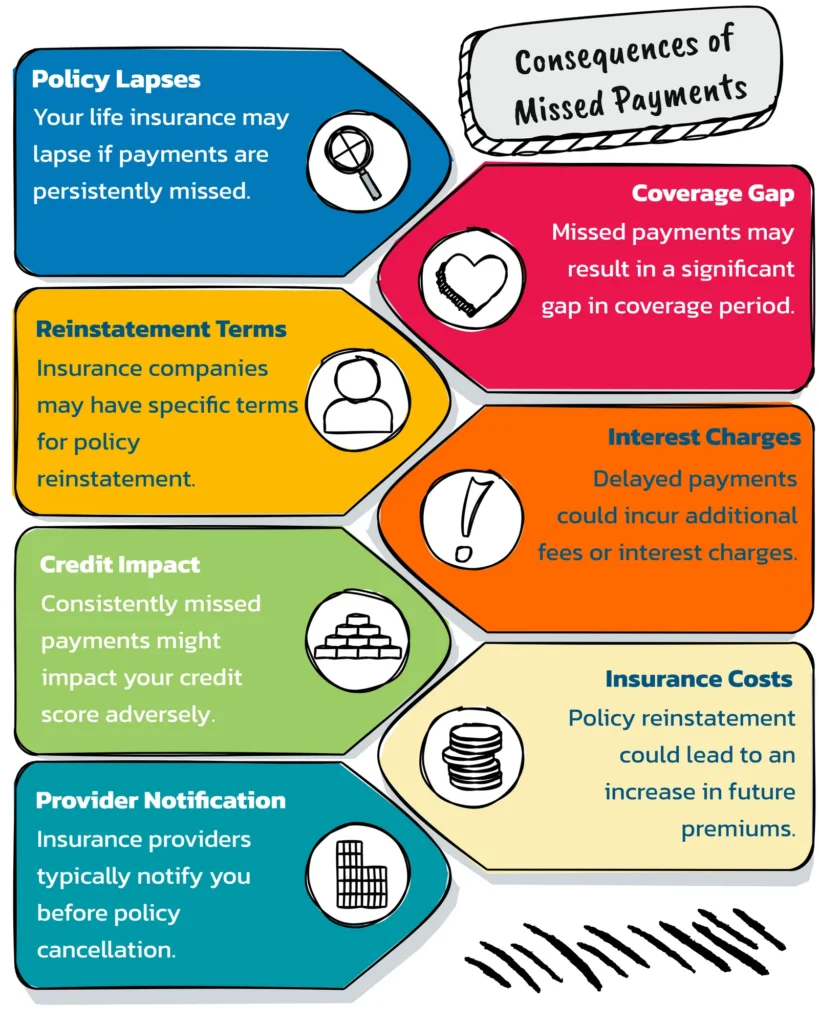

2. Policy Lapse: Loss of Coverage

If you fail to pay the premium even after the grace period, your policy may lapse.

Consequences of a policy lapse:

- No insurance coverage

- Claims may be rejected

- Financial risk shifts back to you

- Loss of accumulated benefits (in some policies)

For example, a lapsed health insurance policy won’t cover hospitalization expenses.

3. Claim Rejection Risk

If an insured event occurs while your policy is lapsed:

- The insurer is not liable to pay the claim

- You may have to bear the full financial burden

This can be especially risky for health and life insurance policies.

4. Revival or Reinstatement of Policy

Many insurers allow you to revive a lapsed policy within a specific time frame.

Revival may require:

- Paying pending premiums

- Late fees or penalties

- Health declaration or medical tests (for life/health insurance)

⏱️ Revival periods can range from 2 to 5 years, depending on the policy.

5. Impact on Bonuses and Benefits

Missing premiums can also affect policy benefits such as:

- No Claim Bonus (NCB) in health insurance

- Loyalty bonuses in life insurance

- Add-on covers and riders

Some benefits may be lost permanently if the policy lapses.

6. Effect on Tax Benefits

Insurance premiums often qualify for tax deductions under applicable income tax laws.

If your policy lapses:

- You may lose future tax benefits

- Past deductions could be reversed in certain cases

What If You Miss Premiums Repeatedly?

Repeatedly missing premium payments can:

- Increase your risk profile

- Make future insurance more expensive

- Reduce insurer trust

- Lead to policy cancellation

This is especially critical for term and health insurance.

How to Avoid Missing Insurance Premium Payments

Here are some simple tips to stay protected:

- ✅ Set auto-debit or standing instructions

- ✅ Use calendar or mobile reminders

- ✅ Choose premium frequency wisely

- ✅ Keep your contact details updated with the insurer

- ✅ Review your policy annually

Can You Buy a New Policy After Missing Payments?

Yes, but:

- You may have to go through fresh underwriting

- Premiums could be higher

- Waiting periods may restart (especially in health insurance)

Reviving an old policy is often better than buying a new one.

Key Takeaways

- Missing insurance premium payments can lead to policy lapse and loss of coverage

- Grace periods provide short-term relief

- Lapsed policies can often be revived, but with conditions

- Timely premium payments protect your financial future

Final Thoughts

Insurance works only when it’s active. Missing premium payments, even unintentionally, can expose you to serious financial risks. Understanding grace periods, revival rules, and consequences can help you take timely action and stay protected.

💡 Tip: Treat insurance premiums like a non-negotiable monthly expense—just like rent or utilities.