Microinsurance is a powerful financial tool designed to protect low-income individuals and vulnerable communities against unexpected risks such as illness, accidents, crop failure, or death. Unlike traditional insurance, microinsurance offers affordable premiums, simple policies, and easy claim processes, making financial security accessible to people with limited income. In developing economies, microinsurance plays a crucial role in financial inclusion and poverty reduction.

What Is Microinsurance?

Microinsurance is a type of insurance specifically created for low-income groups, including daily wage workers, small farmers, street vendors, self-employed individuals, and rural households. These policies cover basic risks at a very low cost, ensuring that people are not pushed deeper into poverty due to sudden financial shocks.

Key Features of Microinsurance

- Low and affordable premiums

- Simple terms and conditions

- Limited but essential coverage

- Quick and easy claim settlement

- Designed for individuals with irregular income

Why Is Microinsurance Important?

Low-income families are often one emergency away from financial distress. Medical expenses, accidents, or natural disasters can wipe out their savings. Microinsurance helps by:

- Providing financial protection during emergencies

- Reducing dependency on loans or moneylenders

- Encouraging financial stability and confidence

- Supporting long-term economic growth

- Promoting social security and inclusion

Types of Microinsurance

Microinsurance products are tailored to meet essential needs. Common types include:

1. Health Microinsurance

Covers basic medical expenses, hospital stays, and treatments at minimal cost.

2. Life Microinsurance

Provides financial support to the family in case of the policyholder’s death.

3. Crop and Agricultural Microinsurance

Protects farmers against losses due to droughts, floods, pests, or crop failure.

4. Accident Microinsurance

Offers compensation in case of accidental injury, disability, or death.

5. Property Microinsurance

Covers small homes, shops, tools, or livestock against damage or loss.

How Microinsurance Works

Microinsurance policies are often distributed through:

- NGOs and self-help groups

- Microfinance institutions (MFIs)

- Cooperative societies

- Government-backed schemes

- Mobile and digital platforms

Premiums are usually collected weekly, monthly, or seasonally to suit irregular income patterns. Claims are processed with minimal documentation, ensuring faster payouts.

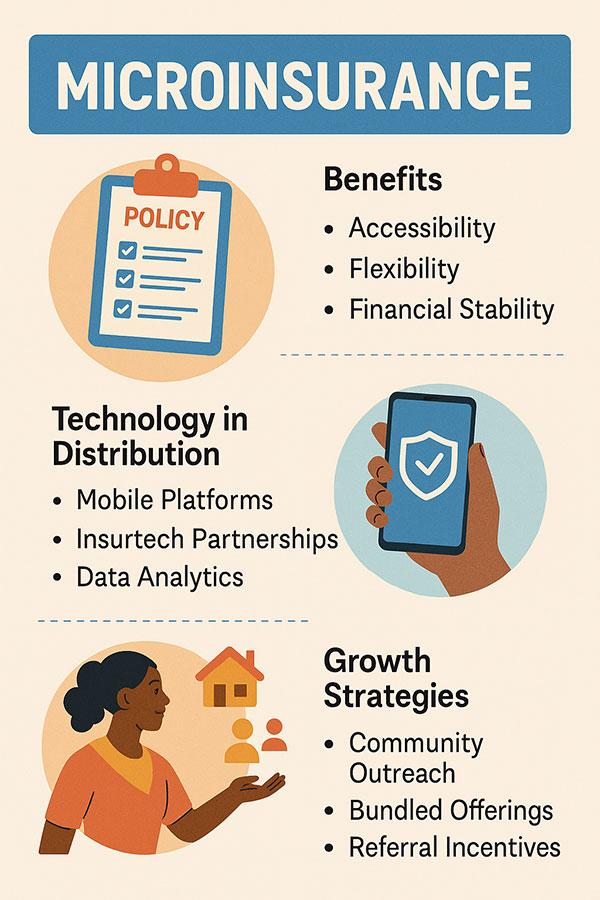

Benefits of Microinsurance for Low-Income Groups

- Affordable protection against everyday risks

- Improves resilience during crises

- Encourages savings and responsible financial behavior

- Reduces poverty-related vulnerabilities

- Enhances trust in formal financial systems

Challenges in Microinsurance

Despite its benefits, microinsurance faces certain challenges:

- Low awareness and financial literacy

- Limited coverage amounts

- Trust issues due to past claim delays

- High operational costs for insurers

- Difficulty reaching remote areas

However, digital technology and mobile-based insurance models are gradually overcoming these barriers.

Role of Technology in Microinsurance

Technology is transforming microinsurance by:

- Enabling mobile-based enrollment and payments

- Using digital wallets for premium collection

- Speeding up claim verification through AI and data analytics

- Increasing reach in rural and remote areas

This makes microinsurance more efficient, transparent, and scalable.

Conclusion

Microinsurance is more than just insurance—it is a lifeline for low-income groups. By offering affordable and accessible coverage, it protects vulnerable communities from financial shocks and helps them build a more secure future. As awareness grows and technology advances, microinsurance will continue to play a vital role in promoting financial inclusion, social security, and sustainable development.

FAQs on Microinsurance

Q1. Who should buy microinsurance?

Anyone with low or irregular income, especially daily wage workers, farmers, and small business owners.

Q2. Is microinsurance expensive?

No, microinsurance is designed to be extremely affordable with low premiums.

Q3. Does microinsurance cover major risks?

It covers essential risks like health issues, accidents, life, and crops, though coverage limits are smaller than traditional insurance.